We now have a working definition of money: money includes both currency and deposits at banks. And while private individuals and firms aren’t permitted to print currency, private actions do influence the supply of money in the economy, because both private individuals and banks affect deposits. In this section, we explain how banks create money as a by-product of their daily business activity. Note that when we refer to “banks,” we are talking about commercial banks, which take in deposits and extend loans. We distinguish commercial banks from investment banks, which serve a different role.

We begin by looking closely at the daily activities at typical banks. After that, we consider how banks influence the money supply.

The Business of Banking

Banks serve two very important roles in the macroeconomy. First, they are middlemen in the market for loanable funds. As we saw in Chapter 23, they provide a way for savers to supply their funds to borrowers without purchasing a financial security. Second, they play a role in creating the supply of money.

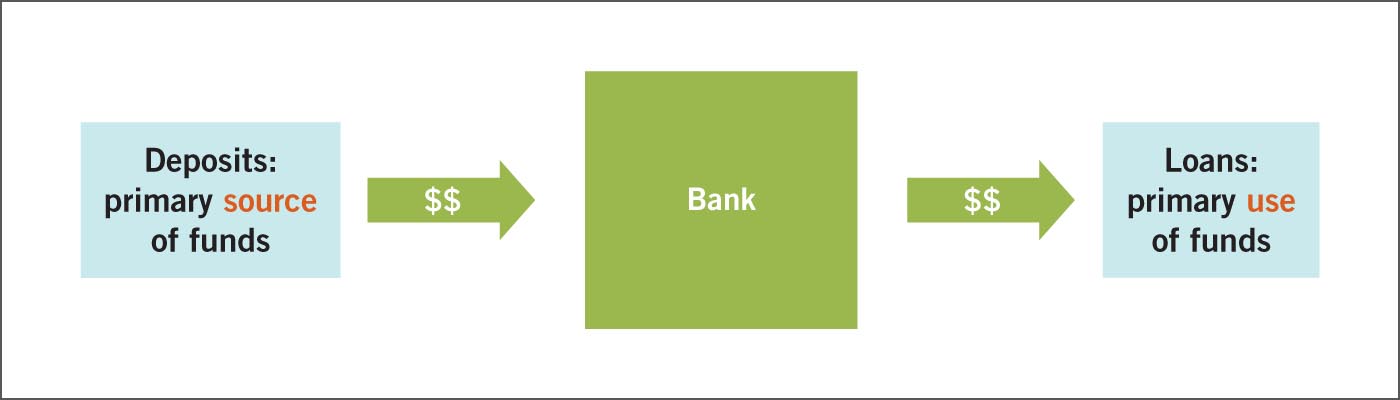

To understand how banks create money, let us consider the functions of a bank, illustrated in Figure 30.2. Banks are go-betweens in the market for loans. They are financial intermediaries; that is, they take in deposits and extend loans. Deposits are the primary source of funds, and loans are the primary use of these funds. Banks can be profitable if the interest rate they charge on loans is higher than the interest rate they pay out on deposits.

FIGURE 30.2

The Business of Banking: Financial Intermediation

The primary function of commercial banks is financial intermediation: they accept deposits and extend loans.

More information

A flowchart depicting financial intermediation. Deposits are the primary source of funds. The money goes into a bank, which in turn sends the money out as loans, the primary use of funds.

FIGURE 30.3

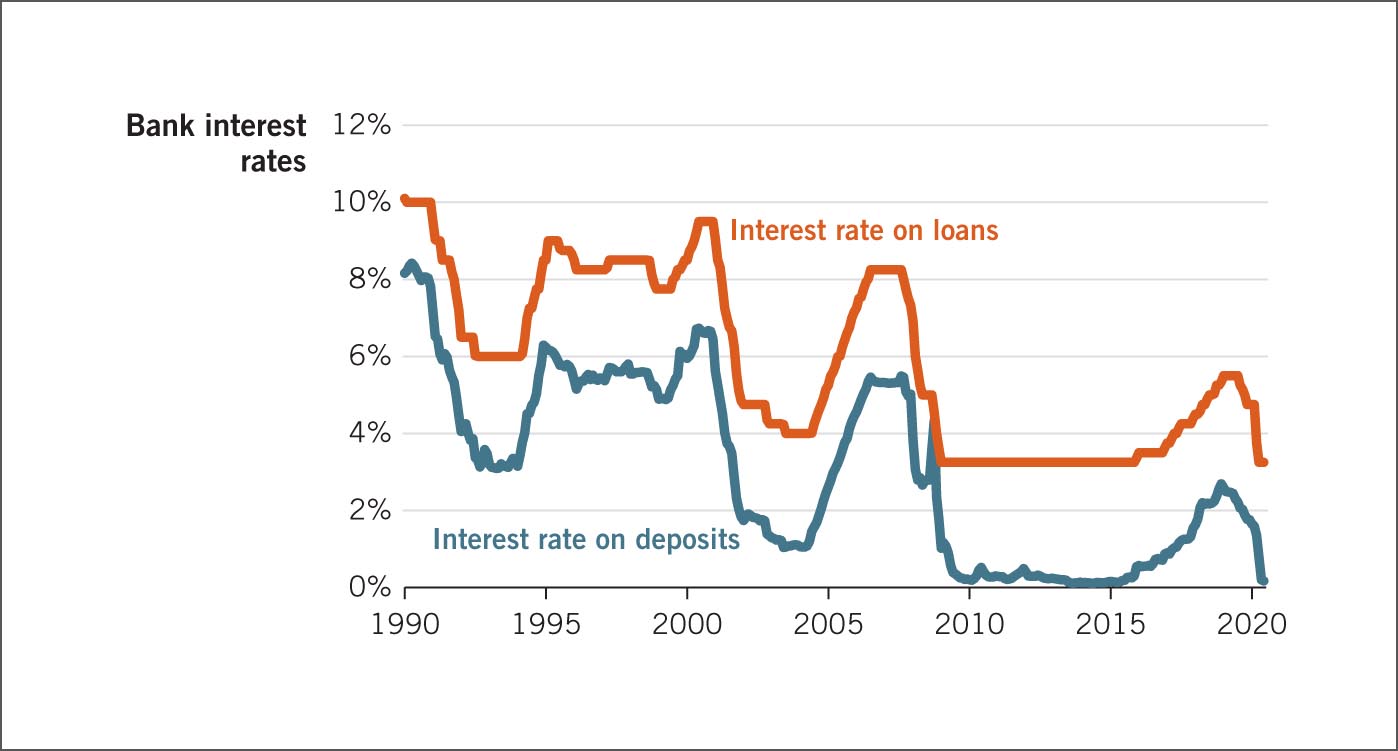

Interest Rates on Bank Deposits versus Loans, 1990–2020

Banks charge more interest for loans than they pay for deposits. The difference pays the banks’ expenses and produces profits.

Source: FRED data, Federal Reserve Bank of St. Louis. The loan interest rate is the average prime interest rate across the United States; the deposit interest rate is the interest rate on three-month certificates of deposit.

More information

A line chart showing interest on loans and interest on deposits for the years 1990 to 2020. The interest rate on deposits starts at 8 percent in 1990. It moves up and down over the years but trends downward. It is at or near zero in 2020. The interest rate on loans mirrors the movement of the interest rate on deposits but is between 2 and 2.5 percent higher.

Figure 30.3 illustrates the gap between interest rates on bank deposits and bank loans for U.S. banks for the period 1990–2020. The two rates go up and down together, but the interest rate on deposits is consistently lower than the interest rate on loans. The difference between the two interest rates helps pay a bank’s operating costs and produces profits.

THE BANK’S BALANCE SHEET

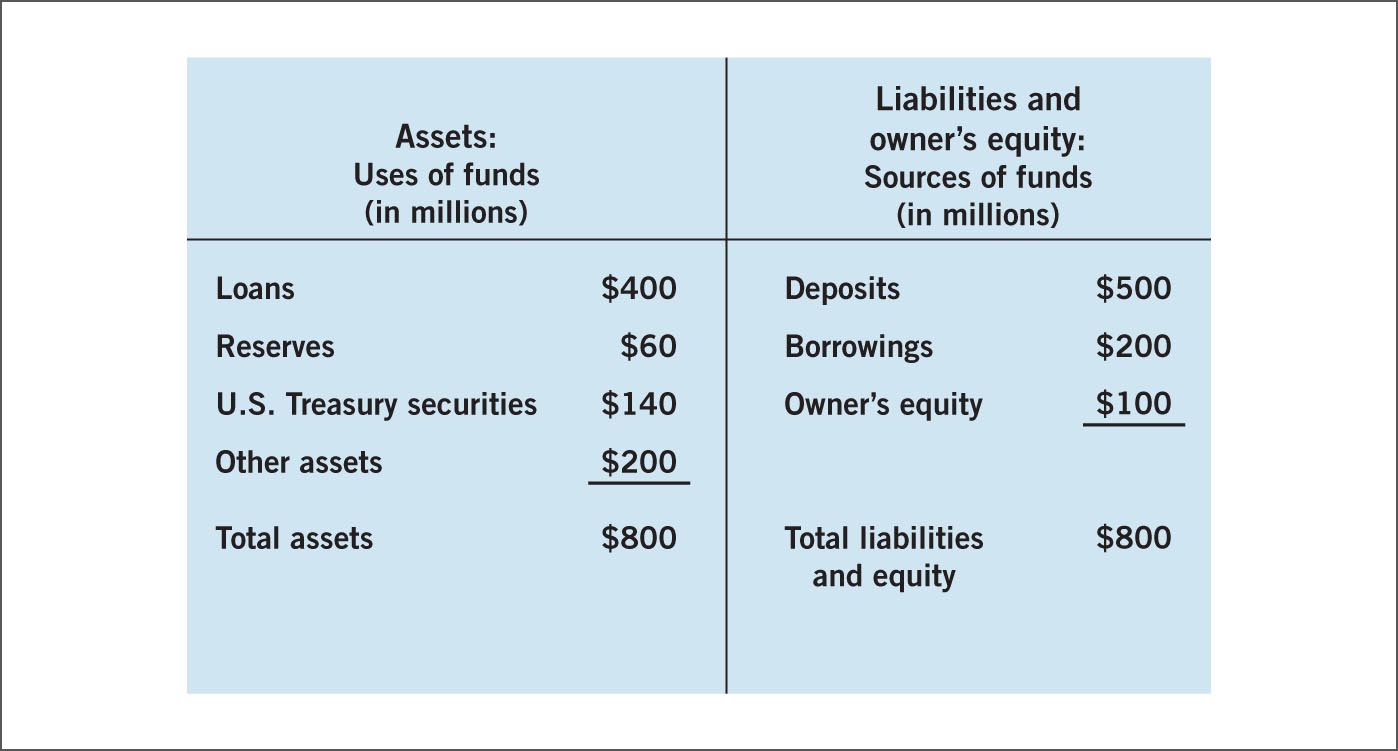

Information about a bank’s financial operations is available in the bank’s balance sheet. A balance sheet is an accounting statement that summarizes a firm’s key financial information. Figure 30.4 shows a hypothetical balance sheet for University Bank. The left side of the balance sheet details the bank’s assets, which are the items the firm owns. Assets indicate how the banking firm uses the funds it has raised from various sources. The right side of the balance sheet details the bank’s liabilities and owner’s equity. Liabilities are the financial obligations the firm owes to others. Owner’s equity (sometimes called shareholders’ equity) is the difference between the firm’s assets and its liabilities. When a firm has more assets than liabilities, it has positive owner’s equity. Overall, the right side of the balance sheet identifies the bank’s sources of funds.

FIGURE 30.4

Balance Sheet for University Bank

A bank’s balance sheet summarizes its key financial information. The bank’s assets are recorded on the left side; this side shows how the bank chooses to use its funds. The sources of the firm’s funds are recorded on the right side; this side shows liabilities and owner’s equity. The two sides of the balance sheet must match for the financial statement to be balanced.

More information

A bank balance sheet, with two columns. In the assets column, the uses of funds are loans, 400 million dollars, reserves, 60 million, U S Treasury securities, 140 million, and other assets, 200 million, which add up to 800 million dollars in total assets. In the column for liabilities and owner’s equity, the sources of funds are deposits, 500 million dollars, borrowings, 200 million, and owner’s equity, 100 million, which add up to 800 million dollars in total liabilities and equity.

As you can see, University Bank has extended $400 million in loans. Many of these loans went to firms to fund investment, but some also went to households to purchase homes, cars, and other consumer items. A second important asset held by banks is reserves. Reserves are the portion of bank deposits set aside and not loaned out. Reserves include both currency in the bank’s vault and funds that the bank holds in deposit at its own bank, the Federal Reserve. Banks also hold U.S. Treasury securities and other government securities as substantial assets in their portfolio. These securities earn interest and carry very low risk. Finally, banks hold other assets, such as physical buildings and furniture.

Turning to the right side of the balance sheet, we look at the major sources of funds for banks. Banks fund their activities primarily by taking in deposits. In fact, the deposits of typical households are the lifeblood of banks. Banks also borrow from other commercial banks and from the Federal Reserve. The third item on the right side of the balance sheet in Figure 30.4 is the owner’s equity in the bank. Because University Bank owns $800 million in total assets but owes only $700 million in liabilities ($500 million in deposits plus $200 million in borrowings), the owners of the bank have $100 million in equity.

In the next section, we look more closely at bank reserves, which play an important role in money creation.

BANK RESERVES

Our modern system of banking is a fractional reserve system. Fractional reserve banking occurs when banks hold only a fraction of deposits on reserve. The alternative is 100% reserve banking. Banks in a 100% reserve system don’t loan out deposits; these banks are essentially just safes, keeping deposits on hand until depositors decide to make a withdrawal.

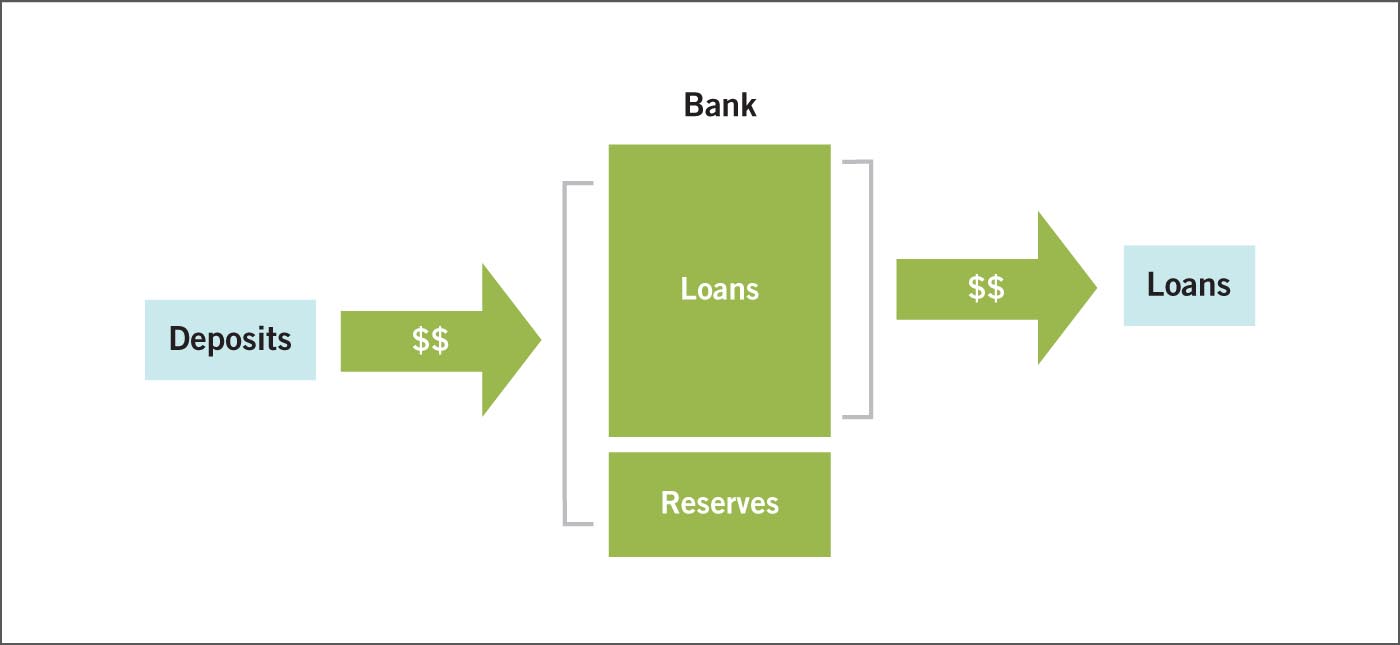

Figure 30.5 illustrates the process of fractional reserve banking. Deposits come into the banks, and banks send out a portion of these funds in loans. In recent years, U.S. banks have typically loaned out 75 to 85% of their deposits, keeping 15 to 25% on reserve. Banks loan out most of their deposits because, as was already mentioned, collecting interest on loans is how banks cover their costs and earn a profit.

Still, banks do hold some deposits on reserve in order to accommodate withdrawals by their depositors. You’d be pretty unhappy if you tried to make a withdrawal from your bank and it didn’t have enough on reserve to honor your request. If word spread that a bank might have difficulty meeting its depositors’ withdrawal requests, it might lead to a bank run. A bank run occurs when many depositors attempt to withdraw their funds from a bank at the same time.

Before 2020, banks were required to hold a certain portion of their deposits in reserve. The required fraction was called the required reserve ratio. For a given bank, the dollar amount of required reserves was required determined by multiplying the required reserve ratio by the bank’s total amount of deposits. In 2020, the Fed switched to a different tool for encouraging banks to maintain reserves, namely paying banks interest on reserves. We discuss this tool later in the chapter. As for the reserve ratio, it is no longer a requirement but is still a useful concept, as we will see.

FIGURE 30.5

Fractional Reserve Banking

In a fractional reserve banking system, banks lend out only a fraction of the deposits they take in. The remainder is set aside as reserves.

More information

A flowchart depicting fractional reserve banking. Deposits flow into a bank. A portion is kept as reserves. The rest flows out again, as loans.

Opportunity cost

THE FDIC AND MORAL HAZARD

Because a bank keeps only a fraction of its deposits on reserve, if all depositors try to withdraw their deposits at the same time, the bank will not be able to meet its obligations. But in a typical day, only a small number of deposits are withdrawn. In the past, when word spread that a bank was unstable and perhaps could not meet the demands of depositors—whether this rumor was true or not—depositors would rush to withdraw their funds, leading to a bank run.

During the Great Depression, bank failures became common. From 1929 to 1933, over 9,000 banks failed in the United States alone—more than in any other period in U.S. history. It is clear that many banks were extending loans beyond their ability to collect and pay depositors in a timely manner. As a result, many depositors lost confidence in the banking system. If you became worried about your bank and were not certain you could withdraw your deposits at some later point, wouldn’t you run to the bank to get your money out?

This is precisely what happened to many banks during the Great Depression. The Hollywood film classic It’s a Wonderful Life (1946) captures this situation perfectly. In the movie, the character George Bailey is set to leave on his honeymoon when the financial intermediary he runs is subject to a run. When a depositor asks for his money back, George tells him, “The money’s not here. Well, your money’s in Joe’s house, that’s right next to yours. And in the Kennedy house, and Mrs. Macklin’s house, and, and a hundred others.” This quote summarizes both the beauty and the danger wrapped up in a fractional reserve banking system. Fractional reserve banking allows access to funds by many individuals and firms in an economy, but it can also lead to instability when many depositors demand their funds simultaneously.

More information

A scene from It’s a Wonderful Life. As panicked depositors crowd into George Bailey’s bank, he offers them money from his own wallet.

To end the bank run, George Bailey offers depositors money from his own wallet.

After the massive rate of bank failures from 1929 to 1933, the U.S. government instituted federal deposit insurance in 1933 through the Federal Deposit Insurance Corporation (FDIC). Deposit insurance now guarantees that depositors will get their deposits back (up to $250,000) even if their bank goes bankrupt. FDIC insurance greatly decreased the frequency of bank runs. Unfortunately, deposit insurance also created what we call a moral hazard situation. Moral hazard is the lack of incentive to guard against risk where one is protected from its consequences. FDIC insurance means that neither banks nor their depositors have an incentive to monitor risk; no matter what happens, they are protected from the consequences of risky behavior.

Consider two types of banks in this environment. Type A banks are conservative, take little risk, and earn relatively low returns on their loans. Type A banks make only very safe loans with very little default risk and, consequently, relatively low rates of return. Type A banks rarely fail, but they make relatively low profit and pay relatively low interest rates to their depositors. In contrast, Type B banks take huge risks, hoping to make extremely large returns on their loans. Type B loans carry greater default risk but also pay higher returns. Type B banks often fail, but the lucky ones—the ones that survive—earn very handsome profits and pay high interest rates on their customers’ deposits.

Moral hazard draws individual depositors and bankers to type B banking. There is a tremendous upside and no significant downside, because depositors are protected against losses by FDIC insurance. This is the environment in which our modern banks operate, which is why many analysts argue that reserve requirements and other regulations are necessary to help ensure stability in the financial industry—especially given that recessions often start in the financial industry.

ECONOMICS IN THE REAL WORLD

TWENTY-FIRST-CENTURY BANK RUN

For a modern example of a bank run, consider England’s Northern Rock Bank, which experienced a bank run in 2007—the first British bank run in over a century. Northern Rock (which is now owned by Virgin Money) had earned revenue valued over $10 billion per year. But extensive losses stemming from investments in mortgage markets led it to near collapse in 2007.

In September of that year, depositors began queuing outside Northern Rock locations because they feared they would not get their deposits back. Eventually, the British government offered deposit insurance of 100% to Northern Rock depositors—but not before much damage had been done. In February 2008, Northern Rock was taken over by the British government because the bank was unable to repay its debts or find a buyer. To make matters worse, there is some evidence that Northern Rock was solvent at the time of the bank run, meaning that stronger deposit insurance could have saved the bank.

In the United States, over 300 banks failed between 2008 and 2011 without experiencing a bank run. (So these banks failed, but the failure did not lead to a bank run.) The individual depositors who funded the risky loans got their money back. So why the bank run in England? The difference is a reflection of the level of deposit insurance offered in the two nations. In England, depositors are insured for 100% of their deposits up to a value of $4,000, then for only 90% of their next $70,000. So British depositors get back a fraction of their deposits up to about $74,000. In contrast, FDIC insurance in the United States offers 100% insurance on the first $250,000.

More information

Depositors queue up outside a Northern Rock Bank, hoping to withdraw money.

Depositors queue outside a Northern Rock Bank location in September 2007.

Creating Money by Multiplying Deposits

We have seen that banks function as financial intermediaries. But as a by-product of their everyday activity, they also create new money. Modern U.S. banks don’t mint currency, but they do create new deposits, and deposits are a part of the money supply.

Money deposited in the banking system leads to more money. To see how, let’s start with a hypothetical example that involves the Federal Reserve, which supplies the currency in the United States. Let’s say that the Federal Reserve decides to increase the money supply in the United States. It prints a single $1,000 bill and drops it out of a helicopter. Let’s say you are the lucky person who finds this brand-new $1,000 bill. If you keep the $1,000 in your wallet, then the money supply increases by only $1,000. But if you deposit the new money in a bank, then the bank can use it to create even more money.

Consider what happens if you deposit the $1,000 into a savings or checking account at University Bank. When you deposit the $1,000, it is still part of the money supply, because both currency and bank deposits are counted in the money supply. You don’t have the currency anymore, but in your wallet you have a debit card that enables you to access the $1,000 to make purchases. Therefore, the deposit still represents $1,000 worth of the medium of exchange.

But University Bank doesn’t keep your $1,000 in reserve; it uses part of your deposit to extend a new loan that earns interest income for the bank. You still have the $1,000 in your account (as a deposit), but someone else receives money from the bank in the form of a loan. Thus, University Bank creates new money by loaning out part of your deposit. You helped the bank in the money creation process because you put your funds into the bank in the first place.

This is just the first step in the money creation process. We’ll now explore this process in more detail, utilizing the bank’s balance sheet. For this example, we make two simplifying assumptions to help understand the general picture:

Assumption 1: All currency is deposited in banks.

Assumption 2: All banks decide to keep 10% of deposits on reserve.

Neither of these assumptions is completely realistic. But let’s work through the example under these conditions, and later we can consider what happens if we relax each assumption.

Consider first how your deposit changes the assets and liabilities of University Bank. The following t-account (an abbreviated version of a firm’s balance sheet) summarizes all initial changes to the balance sheet of University Bank when you deposit your new $1,000 (Assumption 1):

Under Assumption 2, that banks keep 10% of deposits on reserve, University Bank loans out $900 of your deposit. Perhaps the bank loans this amount to a student named Kaitlyn so she can pay her tuition bill. When University Bank extends the loan to Kaitlyn, the money supply increases by $900. That is, you still have your $1,000 deposit, and Kaitlyn now has $900.

Including your initial deposit and this $900 loan, the balance sheet changes at University Bank are summarized in this t-account:

Kaitlyn gives her college the $900, and the college then deposits this amount into its own bank, named Township Bank. But the money multiplication process does not end here. Township Bank also (by Assumption 2 again) loans out 90% of the $900, which is $810. This loan creates $810 more in money supply, so total new money is now $1,000 + $900 + $810 = $1,710. Here are the balance sheet changes at Township Bank:

You can now see that whenever a bank makes a loan, it creates new money. As long as dollars find their way back into the banking system, banks multiply them into more deposits—which means more money. Table 30.1 summarizes this process of money creation. The initial $1,000 deposit ultimately leads to $10,000 worth of money. When monetary funds are deposited into banks, banks can multiply these deposits; and when they do, they create money.

In the end, the impact on the money supply is a large multiple of the initial increase in money. The exact multiple depends on the reserve ratio (rr) the banks decide to maintain. The rate at which banks multiply money when all currency is deposited into banks (Assumption 1) is called the simple money multiplier (mm). The formula for the simple money multiplier is

TABLE 30.1

Money Creation

Assumption 1: All currency is deposited in banks.

Round

Deposit

Assumption 2: Banks hold 10% of deposits on reserve.

1

$1,000

← Initial deposit

Reserve ratio (rr) = 10%

2

900

Initial new money supply = $1,000

3

810

4

729

•

•

•

•

•

•

Sum

$10,000

← Total money

In our example, rr = 0.10, so the multiplier is 1/0.10, which is 10. When the money multiplier is 10, a new $1,000 bill produced by the Federal Reserve can eventually lead to $10,000 in new money.

Of course, in the real world our two assumptions don’t always hold. There is a more realistic money multiplier that relaxes the two assumptions. Consider how a real-world money multiplier would compare with the simple money multiplier. First, if people hold on to some currency (relaxing Assumption 1), banks cannot multiply that currency, so the more realistic multiplier is smaller than the simple money multiplier. On the other hand, when banks hold less on reserve (relaxing Assumption 2), more dollars are multiplied, and the real multiplier is larger than the simple version.

Note that the money multiplier process also works in reverse. When funds are withdrawn from the banking system, these are funds that banks cannot multiply. In effect, the money supply contracts.