How Does the Federal Reserve Implement Monetary Policy?

More information

Jerome Powell shaking hands with Janet Yellen at the Federal Reserve headquarters.

In 2018, Jerome Powell replaced Janet Yellen as the chair of the Fed’s Board of Governors.

There’s a good chance you’ve heard of the U.S. Federal Reserve (Fed), even outside economics class. Jerome Powell, the current Chair of the Fed’s Board of Governors, is one of the most recognized economic policymakers in the world. And while we’ve referred to the Fed periodically throughout this text, now it’s time to examine it closely.

The Many Jobs of the Federal Reserve

The Fed was established in 1913 as the central bank of the United States. The Fed’s primary responsibilities are threefold:

Monetary policy: The Fed is charged with managing monetary policy so as to promote maximum employment and stable prices effectively.

Central banking: The Fed serves as a bank for banks, holding their deposits and extending loans to them.

Bank regulation: The Fed is one of the primary entities charged with ensuring the financial stability of banks.

In this section, we talk about the Fed’s role as central bank and bank regulator. We then look at monetary policy in the remainder of the chapter and into the next chapter.

PRACTICE WHAT YOU KNOW

Fractional Reserve Banking: The Buckeye Bank

More information

A bank loan officer meets with a client. They shake hands across her desk. In the background, people stand in line at the teller counter.

When banks extend loans, the money supply increases.

Use this balance sheet of the Buckeye Bank to answer the questions below. Assume Buckeye Bank is aiming for 10% of deposits in reserves.

BUCKEYE BANK

Assets

Liabilities and equity

Reserves

$50,000

Deposits

$200,000

Loans

120,000

Equity

20,000

Treasury securities

50,000

QUESTION: What is Buckeye’s target level of reserves?

ANSWERANSWER:Buckeye Bank is aiming for 10% of deposits, which is $20,000.

QUESTION: What is the maximum new loan Buckeye Bank will extend?

ANSWERANSWER:Buckeye Bank has $30,000 in extra reserves (reserves beyond its target), so it can extend that total amount in new loans.

QUESTION: How would you rewrite Buckeye Bank’s balance sheet, assuming that this loan is made?

ANSWERANSWER:The only items that would change are reserves, which would decline by $30,000, and loans, which would increase by $30,000.

BUCKEYE BANK

Assets

Liabilities and equity

Reserves

$20,000

Deposits

$200,000

Loans

150,000

Treasury securities

50,000

Equity

20,000

QUESTION: If the Federal Reserve now bought all of Buckeye Bank’s Treasury securities, how large a loan could Buckeye now extend while maintaining its targeted reserve ratio of 10%?

ANSWERANSWER:Buckeye Bank would now have $50,000 in extra reserves, so it could make a loan in this amount.

QUESTION: What would be the maximum impact on the money supply from this Fed action?

ANSWERANSWER:Using the simple money multiplier, we can see that the money supply could grow by as much as $500,000 from this action alone:

CHALLENGE QUESTION: If all banks decide to double their reserve ratios, what happens to the money multiplier?

ANSWERANSWER:The money multiplier falls from 10 to just 5. Banks are not multiplying money as many times, since they are holding more aside on reserve.

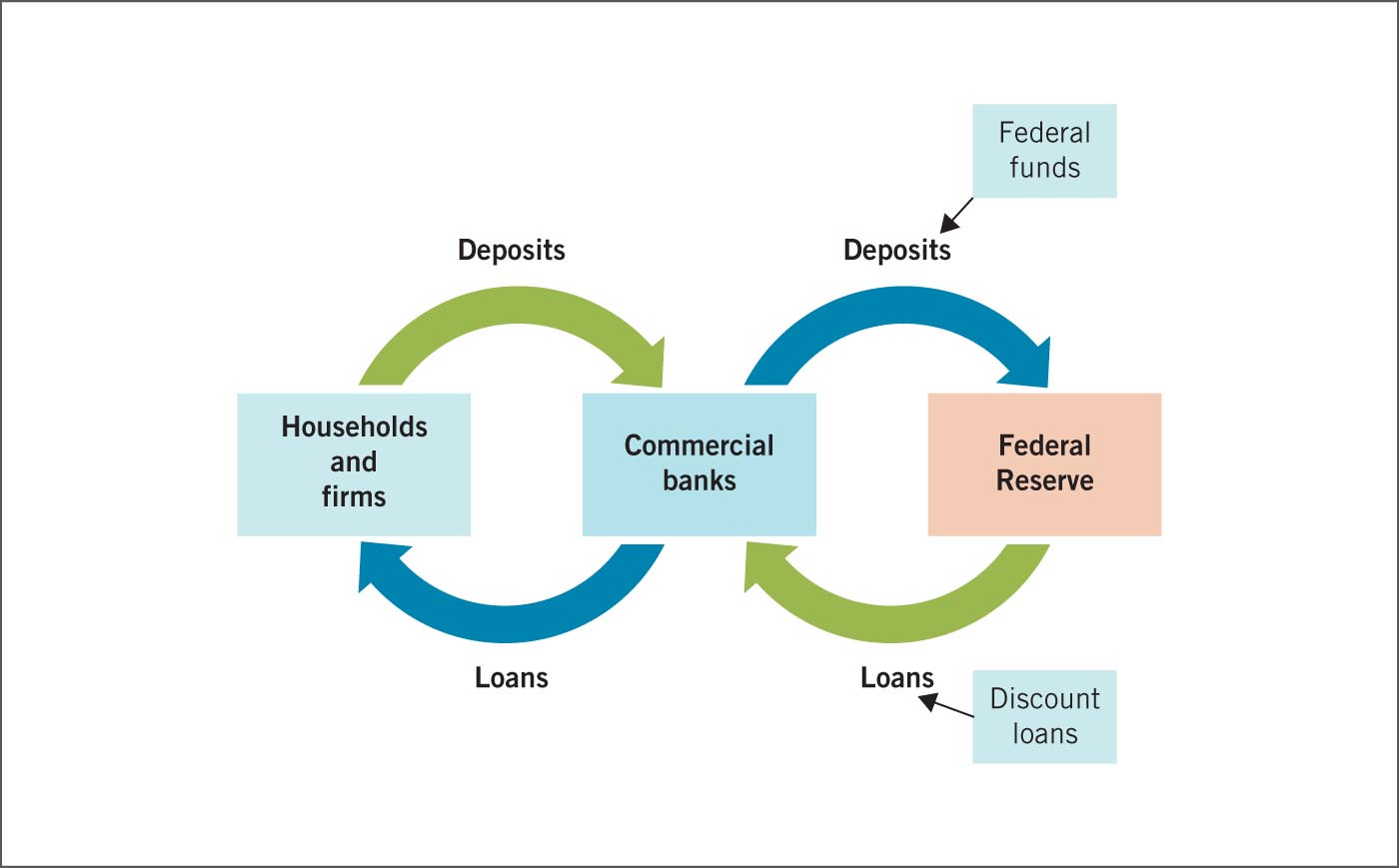

FIGURE 30.6

The Federal Reserve as a Central Bank

The Federal Reserve operates as a central bank for commercial banks. Commercial banks make deposits at the Federal Reserve; these deposits are called federal funds. The Federal Reserve also extends loans to commercial banks; these loans are called discount loans.

More information

A flowchart explains the role of the federal reserve, with households and firms on the left, commercial banks in the middle, and the federal reserve on the right. Households and firms make deposits at commercial banks. The commercial banks, in turn, issue loans to the households and firms but also make deposits at the federal reserve. These deposits are called federal funds. The federal reserve, in turn, issues loans to the banks at the discount rate.

The Fed is a “central bank”—that is, it acts as a “bank for banks.” In its role as central bank, it offers support and stability to the nation’s entire banking system. The first component of this role involves the deposits that banks hold at the Fed. Federal funds are deposits that private banks hold on reserve at the Fed, and, as of 2008, the Fed pays interest on these deposits. The word “federal” seems to denote that the deposits are government funds, but in fact they are private funds held on deposit at a federal agency—the Fed. These deposits are part of the reserves that banks set aside, along with the physical currency in their vaults.

Banks keep reserves at the Fed in part because the Fed clears loans between banks. When banks loan reserves to other banks, these are federal funds loans. The federal funds loans are typically very short term (often overnight), and they enable banks to make quick adjustments to their balance sheets. For example, if our theoretical University Bank dips below its desired reserve level, it can approach Township Bank for a short-term loan. If Township Bank happens to have extra reserves, making a short-term loan enables it to earn additional interest. The interest rate that banks charge each other on interbank loans is known as the federal funds rate. This rate moves up and down based on the borrowing and lending choices of individual banks. The federal funds rate is generally higher than the interest rate banks earn on their reserves at the Fed.

The federal funds rate is one of the most closely monitored interest rates in the world. This is the interest rate that the Fed “targets,” for monetary policy. Because the actual quantity of money in the economy is hard to measure, the Fed monitors conditions in the banking system by watching the federal funds rate (among other indicators). In the next section, we’ll discuss how the Fed acts to push the federal funds rate up and down, depending on macroeconomic conditions.

Figure 30.6 illustrates how the relationship between the Federal Reserve and commercial banks is analogous to the relationship between commercial banks and households and firms. First, households and firms hold deposits at banks, and banks hold deposits at the Fed—these are the federal funds. Second, households and firms take out loans from banks, and banks take out loans from the Fed. The loans from the Fed to the private banks are known as discount loans.

Discount loans are the vehicle by which the Fed performs its role as “lender of last resort.” Given the macroeconomic danger of bank failure, the Fed serves an important role as a backup lender to private banks that find difficulty borrowing elsewhere. The discount rate is the interest rate on the discount loans made from the Fed to private banks. The Fed sets this interest rate because it is a loan directly from a branch of the U.S. government to private financial institutions.

Discount loans don’t often figure prominently in macroeconomics, but in extremely turbulent times, they reassure financial market participants. For example, when many banks were struggling in 2008, financial market participants were assured that troubled banks could rely on the Federal Reserve to fortify failing banks with discount loans. In fact, for the first time in history, other financial firms were allowed to borrow from the Fed. The Fed even extended an $85 billion loan to the insurance company American International Group because it had written insurance policies for financial securities based on failing home mortgages.

Incentives

The Fed also serves as a regulator of individual banks. The Fed monitors the balance sheets of banks with an eye toward limiting the riskiness of the assets the banks hold. One might ask why banks are subject to this kind of regulation. After all, the government doesn’t monitor the riskiness of assets owned by other private firms. However, as we have seen, the interdependent nature of banking firms means that banking problems often spread throughout the entire industry very quickly. In addition, there is the moral hazard problem we discussed earlier: because of deposit insurance, banks and their customers have reduced incentives to monitor the risk of bank assets on their own.

ECONOMICSin theMEDIA

Moral Hazard

Moral Hazard in Wall Street: Money Never Sleeps

More information

Gordon Gecko, played by Michael Douglas, explains the financial facts of life to Jake Moore, played by Shia LaBeouf.

Gordon Gecko understands moral hazard.

WALL STREET: MONEY NEVER SLEEPS

This 2010 film is a sequel to the 1987 movie Wall Street. It focuses on the historical events leading up to and during the financial crisis that began in 2007. One recurring theme in the movie is that some financial firms are “too big to fail.” How can a firm be too big to fail?

If one bank fails, it is unable to repay its depositors and other creditors. This situation puts all the bank’s creditors into similar financial difficulty. If the failing bank is large enough, its failure can set off a domino effect in which bank after bank fails and the entire financial system collapses. If regulators deem a bank too big to fail, they will use government aid to keep the bank afloat.

However, this situation introduces a particularly strong case of moral hazard. After all, banks have incentives to take on risk so they can earn high profits. If we eliminate the possibility of failure by providing government aid, there is almost no downside risk.

In this movie, Gordon Gecko, played by Michael Douglas, defines moral hazard during a public lecture. His definition is this: “When they take your money and then are not responsible for what they do with it.”

Gecko is right: when a financial institution is not required to bear the costs of making poor decisions, it is not legally responsible for mishandling its depositors’ funds.

Monetary Policy Tools

The Federal Reserve has been actively managing the money supply for over a century. But the last two recessions have changed the way the Fed reacts in times of crisis. In addition, because the money supply is difficult to measure, the Fed generally watches market indicators like the federal funds rate to determine the correct stance for monetary policy.

More information

A tall, glass fronted building with an AIG sign.

AIG: The first (and last?) insurance company to get a discount loan from the Fed.

In this section, we discuss the tools the Fed has used to affect the economy, with emphasis on the primary tools used to combat recent recessions. We begin with a relatively new tool, the interest rate paid on bank reserves.

PRACTICE WHAT YOU KNOW

Federal Reserve Terminology

More information

The headquarters building of the Federal Reserve, built of white marble in an austere neoclassical style called stripped classicism.

Loans from the Federal Reserve aren’t called federal funds. They’re called discount loans.

Let’s say the reserves at Buckeye Bank fall below the desired level, so it approaches University Bank for a loan. University Bank agrees to a short-term loan with Buckeye Bank.

QUESTION: What is the name of the funds that private banks like University Bank loan to other private banks (like Buckeye Bank)? What is the interest rate on these loans called?

ANSWERANSWER:The funds are called federal funds. The word “federal” makes it sound as if the funds are a loan from the federal government, but they are not. This wording has been adopted because the loan typically takes place through changes in the two banks’ accounts at their bank, the Federal Reserve. The interest rate is the federal funds rate.

Now assume that Buckeye Bank has made some particularly troublesome loans (perhaps a lot of high-risk mortgage loans) and that all private parties refuse to lend to Buckeye, which then approaches the Fed for a loan to keep its reserves at the desired level.

QUESTION: What is the name of this type of loan? What is the name of the interest rate charged for this loan?

ANSWERANSWER:This is a discount loan, and the interest rate is the discount rate.

INTEREST RATE ON BANK RESERVES

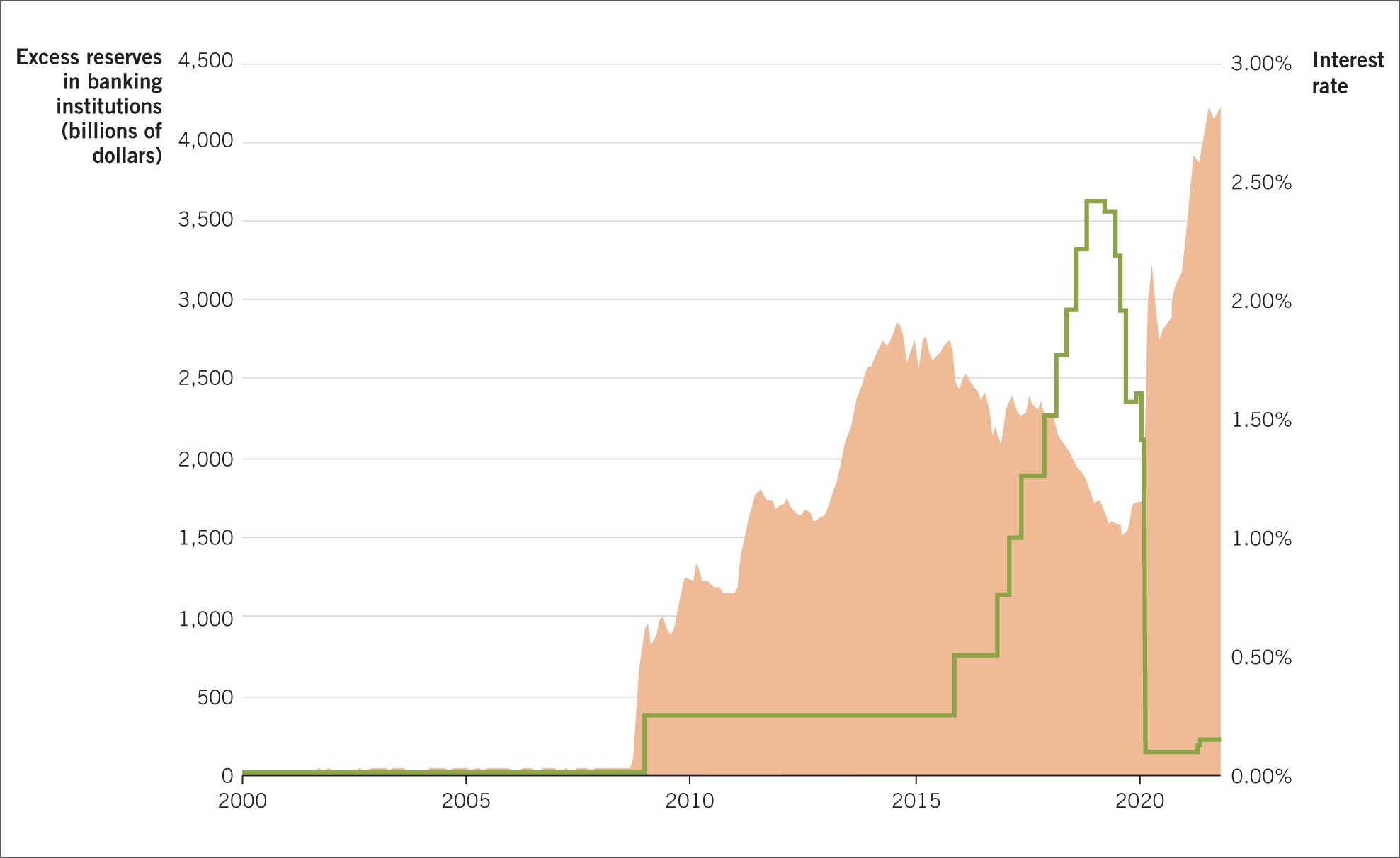

Prior to 2008, bank reserves earned no interest. In that era, there were real opportunity costs to holding reserves, because banks could earn interest on loans or by buying financial securities. But in October 2008, the Federal Reserve began paying interest on bank reserves. The rate of interest, known as the interest on reserve balances (IORB), is now an important policy tool. Immediately, banks started holding more reserves. Figure 30.7 shows total reserves in the banking system from 2000 to 2021 (this is the blue area, which goes with the left axis) along with the IORB (on the right axis). Note that the level of reserves prior to October 2008 was essentially zero. You can clearly see the point when the Fed began paying interest on reserves, as reserves climbed immediately.

Now, the Fed uses this interest rate as its main tool for monetary policy. If the Fed wishes to promote economic activity, it lowers the IORB, as it did in 2020 at the onset of the COVID-19 recession. A reduction in the IORB leads banks to make additional loans, which increases the money supply. This tool can also work in reverse: if the Fed wishes to pull back, it can raise the IORB, causing banks to hold onto more reserves, which dampens the money multiplication process. The Fed did this from 2016 to 2019.

The power of this new tool is still open to debate. As of 2022, banks still held on to significant reserves, even after the interest rate had dropped back down to just 0.15%.

Interest on Bank Reserves

FIGURE 30.7

Bank Reserves and the Interest Rate Paid on Reserves

Total reserves in the banking system (shown as the orange area and measured on the left axis) were essentially zero before the Federal Reserve began paying interest on bank reserves (plotted as the green line and measured on the right axis) in October 2008. During the economic expansion from 2016 to 2019, bank reserves began falling, so the Fed raised the rate of interest on reserve balances (IORB). When the COVID-19 recession began in March 2020, the Fed lowered the IORB to just 0.15%.

More information

A chart showing the Bank reserves and Interest rate paid on reserves from 2000 to 2022. With the vertical scales shown, both bank reserves and interest on reserves are practically zero up to 2009. That year, the interest rate moved up to 0.25% while bank reserves jumped up and continued climbing, eventually peaking at about 2.75 trillion dollars in 2014. As reserves came back down over the following years, the interest rate shot up. In 2019, reserves were back down to 1.5 trillion dollars while interest on reserves stood at just under 2.5 percent. At that point, the trends reversed. The interest rate plummeted while bank reserves skyrocketed. In 2022, bank reserves stood at 4.2 trillion dollars, while the interest on reserves was at about 0.1 percent.

OPEN MARKET OPERATIONS

The Fed can also insert money directly into the economy. As a thought experiment, consider the following three possibilities and see if you can guess which is actually used:

Drop money out of a helicopter.

Distribute $50,000 in new $100 bills to every private bank.

Use new money to buy something in the economy.

If you chose option 3, you are correct. Open market operations involve the purchase or sale of bonds by a central bank. When the Fed wants to increase the money supply, it buys securities; in contrast, when it wishes to decrease the money supply, it sells securities. In Chapter 23, we introduced the U.S. Treasury security as a special bond asset. Normal or “traditional” open market operations involve buying and selling short-term (less than one year) Treasury securities.

In principle, the Fed could realize its desired effects through buying any goods and services—real estate, fine art, or, for that matter, tons of coffee and bagels. It would be as if the Fed created a batch of new currency and then went shopping. When it was done shopping, it would leave behind all the new currency in the economy. Whatever it bought during its shopping spree would become an asset on the Fed’s balance sheet.

There are at least two good reasons why the Fed chooses the Treasury security market for open market operations. First, the Fed’s goal is to get the funds directly into the market for loanable funds. In this way, financial institutions begin lending the new money, and it quickly moves into the economy. Second, a typical day’s worth of open market operations might entail as much as $20 billion in purchases. Imagine being the manager of a bagel shop in Washington, D.C., and having the Fed call in a request for $20 billion worth of bagels. That order would be impossible to fill. But the market for U.S. Treasuries is big enough to accommodate this level of purchases seamlessly. The daily volume in the U.S. Treasury market is over $500 billion, so the Fed can buy and sell without difficulty.

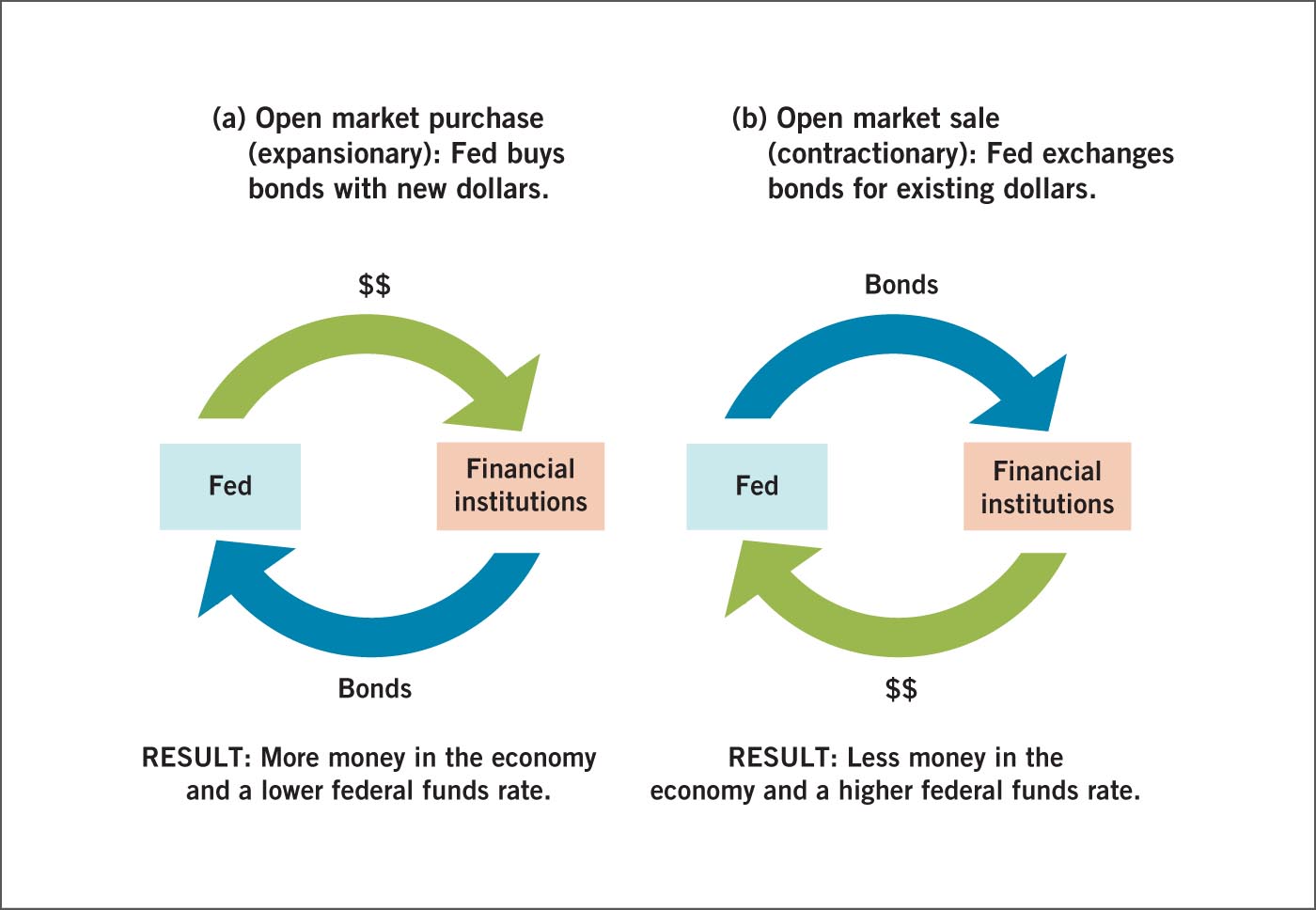

Figure 30.8 summarizes how open market operations work. When the Fed buys Treasury securities held by financial institutions (panel [a]), the Fed pays for those bonds using money it creates. The result is more money circulating in the economy, and this shows up as a reduction in the federal funds rate. On the flip side, when the Fed sells bonds to financial institutions (panel [b]), the money it receives in exchange is taken out of the economy, leaving less money in circulation and a higher federal funds rate. In reality, the Fed undertakes open market operations every business day. Typically, it aims to keep market conditions exactly as they were the day before. But the Fed also uses open market operations to increase the money supply to offset recessions.

FIGURE 30.8

Open Market Operations

In open market purchases, the Fed buys bonds from financial institutions. This action injects new money directly into financial markets. In open market sales, the Fed sells bonds back to financial institutions. This action takes money out of financial markets.

More information

A flowchart depicting two types of open market operation. On the left, the Fed buys bonds with new dollars from financial institutions. The result of this expansionary action is more money in the economy and a lower federal funds rate. On the right, the Fed sells bonds and receives existing dollars from financial institutions. The result of this contractionary action is less money in the economy and a higher federal funds rate.

Starting in 2008, with the economy in the throes of the Great Recession, the Federal Reserve began experimenting with a new variation of open market operations, which has come to be known as quantitative easing. Open market operations typically involve buying and selling short-term Treasury securities—that is, bonds that mature in less than a year. In quantitative easing, the central bank buys longer-term Treasury securities and other types of securities, specifically targeting certain markets. During the Great Recession, for example, the Fed bought mortgage-backed securities that were considered “toxic assets,” meaning assets loaded with risk that could destabilize private markets.

The quantitative easing programs of the Great Recession injected almost $2 trillion in new funds into targeted sectors of the economy. The reason for this move, unprecedented in size and scope, was that conventional open market securities purchased by the Fed had already pushed the federal funds rate down to zero. Reaching the limits of traditional monetary policy, the Fed had to get inventive. But this new strategy, of targeting particular markets for injections of money, caught on. The Fed decided that loans, too, could be targeted to specific industries. We now turn to that development.

THE DISCOUNT WINDOW AND NEW LENDING FACILITIES

Earlier in this chapter, we discussed the Fed’s use of discount loans to support struggling private banks and keep them from failing. The banks obtain these loans at the Fed’s discount window, as it’s called, and the rate the private banks pay on these loans is known as the discount rate. In the past, the Fed would increase the discount rate to discourage borrowing by banks and to decrease the money supply, and it would decrease the discount rate to encourage borrowing by banks and to increase the money supply. These days, instead of being actively managed, the discount rate is generally pegged near the federal funds rate. However, the discount window is still a critical safety net for struggling banks.

The Fed doesn’t just lend to banks. It also lends directly to private financial institutions. Until recently, this was an extremely minor part of the Fed’s overall involvement with the economy. However, direct Fed lending has expanded in both size and scope since the beginning of the Great Recession. This is the second major recent innovation in monetary policy (along with the active use of the IORB). In late 2007 and early 2008, several specific financial industries were in danger of collapse, such as the market in mutual funds and the market in commercial paper (short-term corporate bonds, essentially). Had these industries suffered a wave of bankruptcies, millions of savers would have lost their money. To keep that from happening, the Fed began lending extensively to firms in those markets, through lending facilities set up for that purpose. These early lending facilities were, in effect, discount windows for private financial firms.

More information

A hospitalized COVID patient. The man wears an oxygen mask. A caregiver in head to toe protective gear is taking his temperature with an infrared thermometer.

The Fed’s new lending facilities helped to sustain hospitals that were hit particularly hard by COVID-19.

During the 2020 coronavirus recession, new lending facilities were established to stabilize endangered firms in other industries besides just the financial sector. The Municipal Liquidity Facility provided loans to state and local governments that had seen spending on unemployed workers go up even as tax revenues went down. A second group of facilities, collectively called the Main Street Lending Program, issued loans to small and medium-sized businesses hit hard by shutdowns and social distancing requirements. The Main Street program also extended loans to hospitals and nonprofits.

Traditional Fed action would have been to increase (or decrease) the money supply for the economy as a whole, to increase (or decrease) aggregate demand. This new monetary policy, carried out via lending facilities, is different. However, the basic concept of lending facilities isn’t new at all. It’s just an evolution of the discount window, which has been in place since the inception of the Fed in 1913.

RESERVE REQUIREMENTS

In the past, the Fed also made use of reserve requirements to administer monetary policy. In March 2020, however, the Fed announced that it would no longer require banks to set aside a portion of deposits on reserve. Historically, though, this was an important tool that the Fed used to affect the money multiplier, and it is still used by many other nations. When the Fed lowered the required reserve ratio, the money multiplier increased. When it raised the required reserve ratio, the money multiplier fell.

For example, consider what would happen if the Fed lowered the required reserve ratio to 5% from 10%. This action alone could have doubled the money multiplier. Lowering the required reserve would mean that banks could loan out a larger portion of their deposits, enabling them to create money by multiplying deposits to a greater extent.

This tool was not as precise or predictable as open market operations. Because small changes in the money multiplier could lead to large swings in the money supply, changing the reserve requirement caused the money supply to change too much. In addition, changing reserve requirements also had unpredictable outcomes because the overall effects depended on the actions of banks. It was possible that the Fed would lower the reserve requirement to 5% and banks would not change their reserves. For these reasons, the reserve requirement had not been used for monetary policy since 1992. In addition, as part of the March 2020 response to the coronavirus crisis, the Fed completely eliminated reserve requirements, hoping this would get banks to lend aggressively.

Table 30.2 summarizes the Fed’s monetary policy tools. The tools developed recently are highlighted in orange.

TABLE 30.2

Federal Reserve Tools for Monetary Policy

1. Interest on reserve balances (IORB)

2. Open market operations

Includes quantitative easing

3. Discount window

Includes special lending facilities

Monetary Policy

DATA SNAPSHOT

Show Me the Money!

The interest rate on reserve balances (IORB) is the Fed’s newest monetary policy tool. Generally, when the economy is doing well (the unemployment rate is dropping), the Fed raises the IORB. When the economy is doing poorly (unemployment rates are rising), the Fed lowers the IORB.

DYNAMIC DATA FIGURE

More information

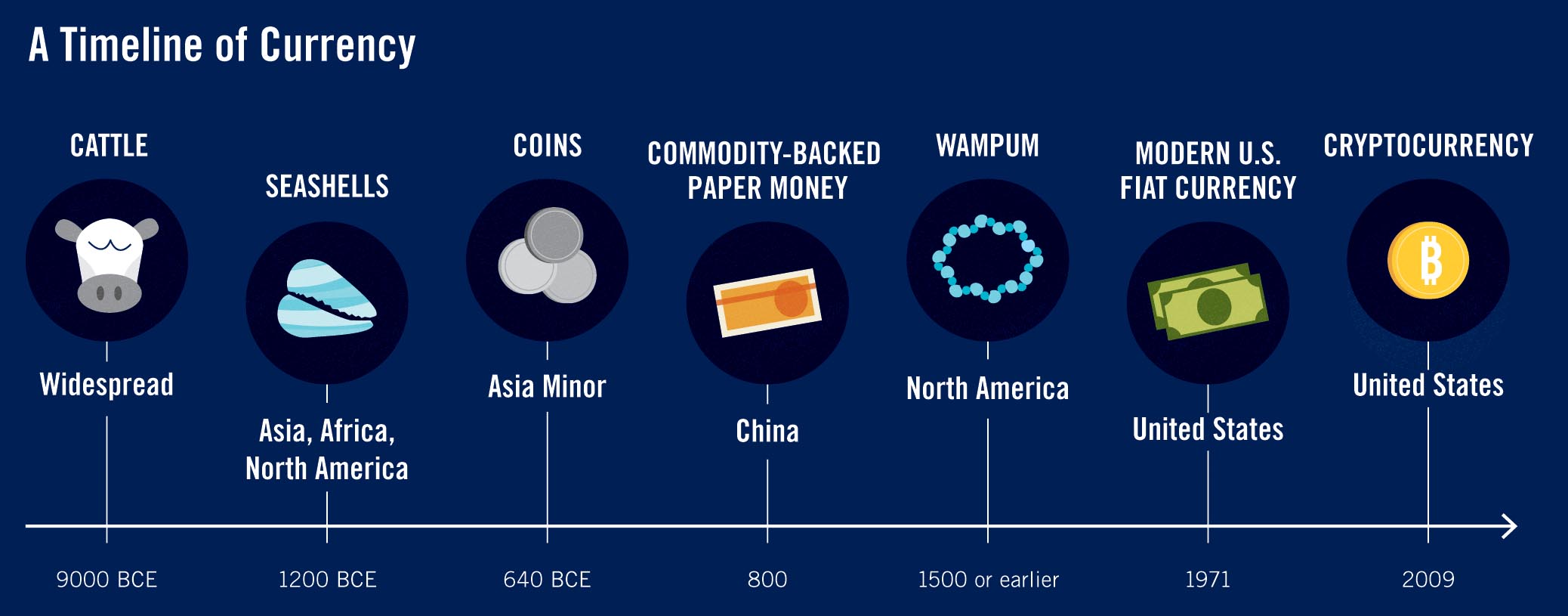

An infographic titled Show Me the Money! In the upper portion, a chart shows the I O R B and the unemployment rate for the years 2007 to 2022. The I O R B was below 0.5% up to 2016 but then started rising, peaking above 2.25% in 2019 before dropping back down near zero. In mid 2022 it jumped back up above 0.75%. The unemployment rate stood just above 4% in 2007, rose to 10% at the end of the 2007 to 2009 recession, then gradually declined back below 4%, with a brief, temporary spike above 14% during the COVID 19 recession. The lower portion is a timeline of currency. Events include the widespread use of cattle as a medium of exchange, as far back as 9000 B C E, seashells in 1200 B C E, and coins in 640 B C E. These were followed by commodity-backed paper money in China in the year 800, Wampum in North America in 1500 or earlier, modern U S fiat currency in 1971, and cryptocurrency in 2009. The two review questions are 1. When did the Federal Reserve begin paying interest on bank reserves? And 2. Why did the Fed lower the I O R B rate so drastically at the beginning of 2020?

REVIEW QUESTIONS

When did the Federal Reserve begin paying interest on bank reserves?

Why did the Fed lower the IORB rate so drastically at the beginning of 2020?

The federal funds rate is the interest rate on loans between private banks. This is the main interest rate that the Fed targets (pushes up and pulls down, depending on economic conditions), because it gives the Fed a strong indicator of the level of money in the economy.

ANSWER

ANSWER ANSWER: Buckeye Bank is aiming for 10% of deposits, which is $20,000.

ANSWER: Buckeye Bank is aiming for 10% of deposits, which is $20,000.